transcribed by Liz Reedy

transcribed by Liz Reedy

To view Gary Taubes’ 1 hour and 22-minute YouTube video, please click here.

Part 4 continues beginning at 38:43

What if Roald Dahl and Michael Pollan are right that the taste of sugar on the tongue can be a kind of intoxication? Doesn’t it suggest that the possibility that sugar itself is an intoxicant, a drug? Imagine a drug that can do this to us, that can infuse us with energy and can do so when taken by mouth. It doesn’t have to be injected, smoked or snorted for us to experience its sublime and soothing effects.

Imagine that it mixes well with virtually every food and particularly liquids. Imagine that when given to infants it provokes a feeling of pleasure so profound and intense that its pursuit becomes a driving force throughout their lives.

By the way, when I put together this thought experiment that I’m about to read, I never thought I’d ever be able to use it in a book. I thought that if I put this in my first chapter it gives away my hand so profoundly that no one will ever think I was balanced or unbiased. And then I sent it to a colleague of mine who is one of the best scientists I know. He said, “If you don’t use this then you’re crazy.”

Overconsumption of this drug has long-term side effects but there are none in the short-term. There is no staggering or dizziness, no slurring of speech, no passing out or drifting away, no heart palpitations or respiratory distress.

When it is given to children, its effects may be only more extreme variations of the apparently natural emotional roller coaster of childhood. From the initial intoxication to the tantrums and whining that may or may not be withdrawal a few hours later. More than anything, our imaginary drug makes children happy, at least during the period in which they’re consuming it.

It calms their distress, eases their pain, focuses their attention and then leaves them excited and full of joy until the dose wears off. The only downside is that children will come to expect another dose, and perhaps demand it on a regular basis.

I should have said this book was also informed by the fact that I am a parent of two pre-adolescent boys. Michael Pollan said to me at lunch one day that moderating your children’s sugar intake is one of the primary responsibilities of adulthood. I borrow from Michael there as well, but I don’t quote him.

How long would it be before parents took to using our imaginary drug to calm their children when necessary, to alleviate pain, to prevent outbursts of unhappiness, or to distract their attention? And, once the drug became identified with pleasure, how long before it would be used to celebrate birthdays, a soccer game, good grades in school?

How long before it would become a way to communicate love and celebrate happiness? How long before no gathering of family and friends was complete without it, before major holidays and celebrations were defined in part, by the use of this drug to ensure pleasure? How long would it be before the underprivileged of the world would happily spend what little money they had on this drug rather than on nutritious meals for their families?

How long would it be before this drug, as the anthropologist, Sidney W. Mintz said about sugar, demonstrated, “A near invulnerability to moral attack.” How long before writing a book such as this one was perceived as a nutritional equivalent to stealing Christmas?

I wanted to call this book Stealing Christmas: The Case Against Sugar and just lay it out there. I understand the Grinch-like aspect of what I’m doing; I’m not blind to it. It’s another way of saying that I’m not an idiot. But my editor preferred otherwise. When I would tell people the title of my book, a surprising number of them didn’t get the Grinch reference. Maybe Dr. Seuss hasn’t permeated our lives quite as much as I thought.

What is it about the experience of consuming sugar and sweets, particularly during childhood that invokes so readily the comparison to a drug? I have children, still relatively young, and I believe raising them would be a far easier job if sugar and sweets were not an option, if managing their sugar consumption, as Michael Pollan said (but I’m not quoting here), did not seem to be a constant theme in our parental responsibilities.

Even those who vigorously defend the place of sugar and sweets in modern diets, “An innocent moment of pleasure, a balm on the distress of life,” as the British journalist Tim Richardson has written, acknowledge that this dose does not include allowing children to eat as many sweets as they want at any time and that, “Most parents would want to ration their children’s sweets.”

Well, why is it necessary? Children collect many things: Pokémon cards, Star Wars paraphernalia, Dora the Explorer backpacks, and many foods taste good to them. What is it about sweets that makes them so uniquely in need of rationing? Which is another way of asking whether the comparison to drugs and abuse is a valid one.

This is of more than academic interest because the response of entire populations to sugar has been effectively identical to that of children. Once populations are exposed, they consume as much sugar as they can easily procure, although there may be natural limits in that culture about current attitudes about food.

The primary barrier to more consumption, up to the point where populations become obese, diabetic and perhaps even beyond, has tended to be availability and price. This includes in one study, sugar-intolerant Canadian Inuit who lacked the enzyme necessary to digest the fructose component of sugar, and yet continued to consume sugary beverages and candy despite “the abdominal distress that it brought them.”

As the price of a pound of sugar has dropped over the centuries, from the equivalent of 360 eggs in the 13th century to 2 eggs in the early decades of this one, the amount of sugar consumed has steadily, inexorably climbed.

In 1934, while sales of candy continued to increase during the Great Depression, the New York Times commented, “The depression proved that people wanted candy and that as long as they had any money at all they would buy it.”

During those brief periods of time during which sugar production surpassed our ability to consume it, the sugar industry and the purveyors of sugar-rich products have worked diligently to increase demand and at least until recently have succeeded.

The critical question which scientists debate, is what journalist and historian Charles C. Mann has eloquently put it, is whether sugar is actually an addictive substance or do people just act like it is. The question is not easy to answer. Certainly, people and populations have acted as though sugar is addictive, but science provides no definitive evidence.

Until recently, nutritionists studying sugar did so from the natural perspective as viewing sugar as a nutrient, a carbohydrate and nothing more. They occasionally argued about whether or not it might play a role in diabetes or heart disease, but not about whether it triggered a response in the brain or body that made us want to consume it in excess. That was not their area of interest.

The few neurologists and psychologists interested in probing the sweet tooth phenomenon or why we might need to ration our sugar consumption so as not to eat it to excess, did so typically from the perspective of how these sugars compared to other drugs of abuse, in which the mechanism of addiction is now relatively well understood.

Lately, this comparison has received more attention as the public health community has looked to ration our sugar consumption as a population and has thus considered the possibility that one way to regulate these sugars, as with cigarettes, is to establish that they are indeed addictive. These sugars are very likely unique in that they are both a nutrient and a psychoactive substance with some addictive characteristics.

Historians have often considered that the sugar-as-a-drug metaphor to be an apt one. “That sugars, particularly highly refined sucrose, produce peculiar physiological effects is well known,” wrote the late Sidney Mintz, whose 1985 book, Sweetness and Power, is one of two seminal English-language histories of sugar, on which other and more recent writers on this subject, myself included, heavily rely.

But these effects are neither as visible nor as long-lasting as those of alcohol or caffeinated beverages, “The first use of which can trigger rapid changes of respiration, heartbeat, skin color, and so on.” Mintz has argued that a primary reason that through the centuries sugar has escaped religious-based criticism for the kind pronounced on tea, coffee, rum, and even chocolate is that whatever conspicuous behavioral changes may occur when infants consume sugar, it did not cause the kind of “flushing, staggering, dizziness, euphoria, changes in the pitch of the voice, slurring of speech, visibly intensified physical activity or any of the other cues associated with the ingestion” of these other drugs.

As this book will argue, sugar appears to be a substance that causes pleasure with a price that is difficult to discern immediately and paid in full in the years or decades later. With no visible, directly noticeable consequence as Mintz says, questions of “long term nutritive or medical consequences went unasked and unanswered.” Most of us today will never know if we suffer even subtle withdrawal symptoms from sugar because we never go long enough without sugar to find out.

Mintz and other sugar historians consider the drug comparison to be so fitting in part because sugar is one of the handful of “drug foods,” to use Mintz’s term, that came out of the tropics, and on which European empires were built from the 16th century onward, the others being tea, coffee, chocolate, rum and tobacco.

Its history is intimately linked to that of these other drugs. Rum is, of course, distilled from sugar cane, whereas tea, coffee and chocolate were not consumed with sweeteners in their regions of origin.

Actually, when the conquistadors discovered the Aztecs eating chocolate in Mexico, in their march and fully confident of their devastation of the people, the Aztecs were mixing it with chili peppers. The conquistadors tried it and said it “tasted awful and they wouldn’t feed it to their pigs.” So, they shipped it back to Europe anyway, and they started mixing it with sugar. Within about 50 years, hot chocolate had become the morning and afternoon drink for the Spanish aristocrats.

In the 17th century, once sugar was added as a sweetener, and prices allowed it, the consumption of these substances in Europe exploded. Sugar was used to sweeten liquors and wine in Europe as early as the 14th century. Even cannabis preparations in India and opium-based wines and syrups included sugar as a major ingredient.

Kola nuts, containing both caffeine and traces of a milder stimulant called theobromine, became a produce of universal consumption in the late 19th century, first as a cocoa-infused wine in France, and then as the original mixture of cocaine and caffeine of Coca-Cola, with sugar added to mask the bitterness of the other two substances. [For more information about kola nuts, please click here and here.]

Stop 49:31 and to be continued

The following is a reprint of a letter of the Editor from Ron Iverson, President of the National Association of Medicare Supplement and Medicare Advantage Producers.

The following is a reprint of a letter of the Editor from Ron Iverson, President of the National Association of Medicare Supplement and Medicare Advantage Producers. by Robert H Lustig, MD, MSL

by Robert H Lustig, MD, MSL Note from Lance: This is a reprint of an article by Dr. Sears with my comments after.

Note from Lance: This is a reprint of an article by Dr. Sears with my comments after. by Ron Iverson, President of the National Association of Medicare Supplement and Medicare Advantage Producers. Inc. and Lance D. Reedy

by Ron Iverson, President of the National Association of Medicare Supplement and Medicare Advantage Producers. Inc. and Lance D. Reedy By Lance D. Reedy

By Lance D. Reedy Note: This is a reprint of an article we originally published in October 2015.

Note: This is a reprint of an article we originally published in October 2015.

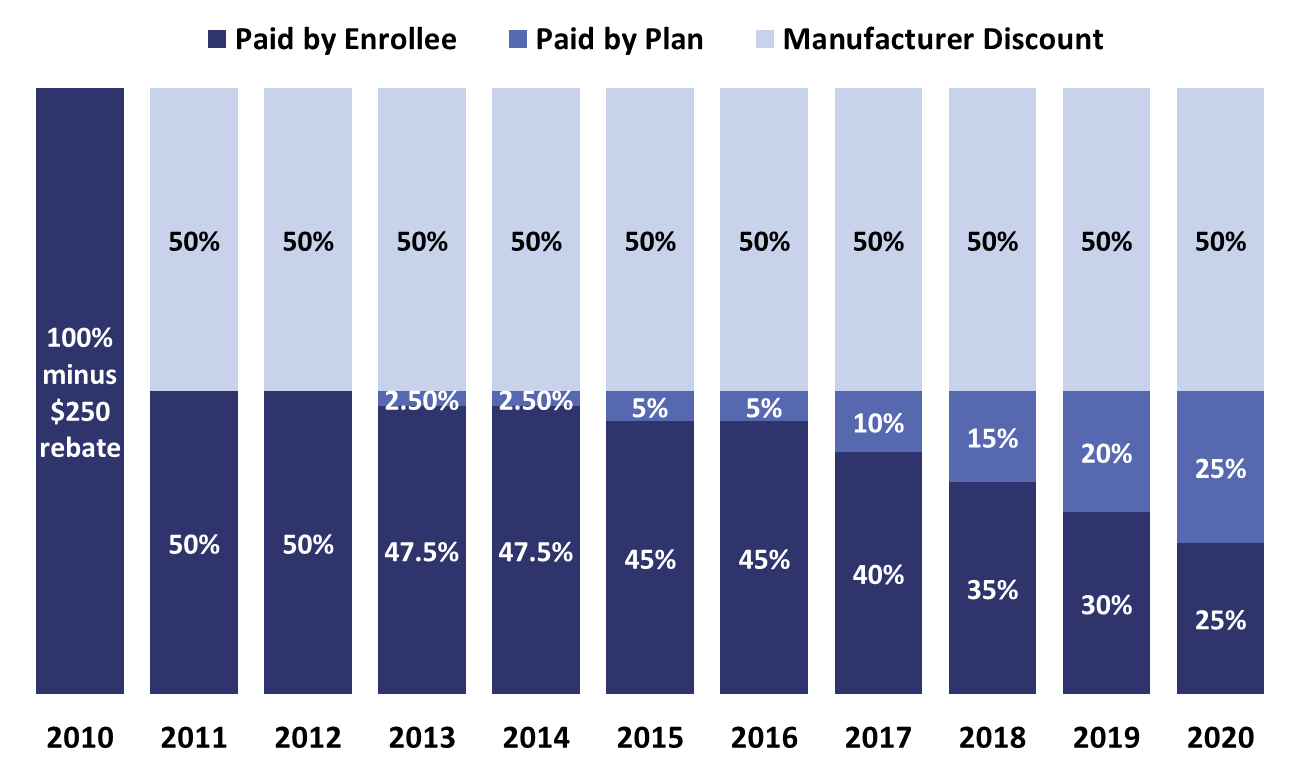

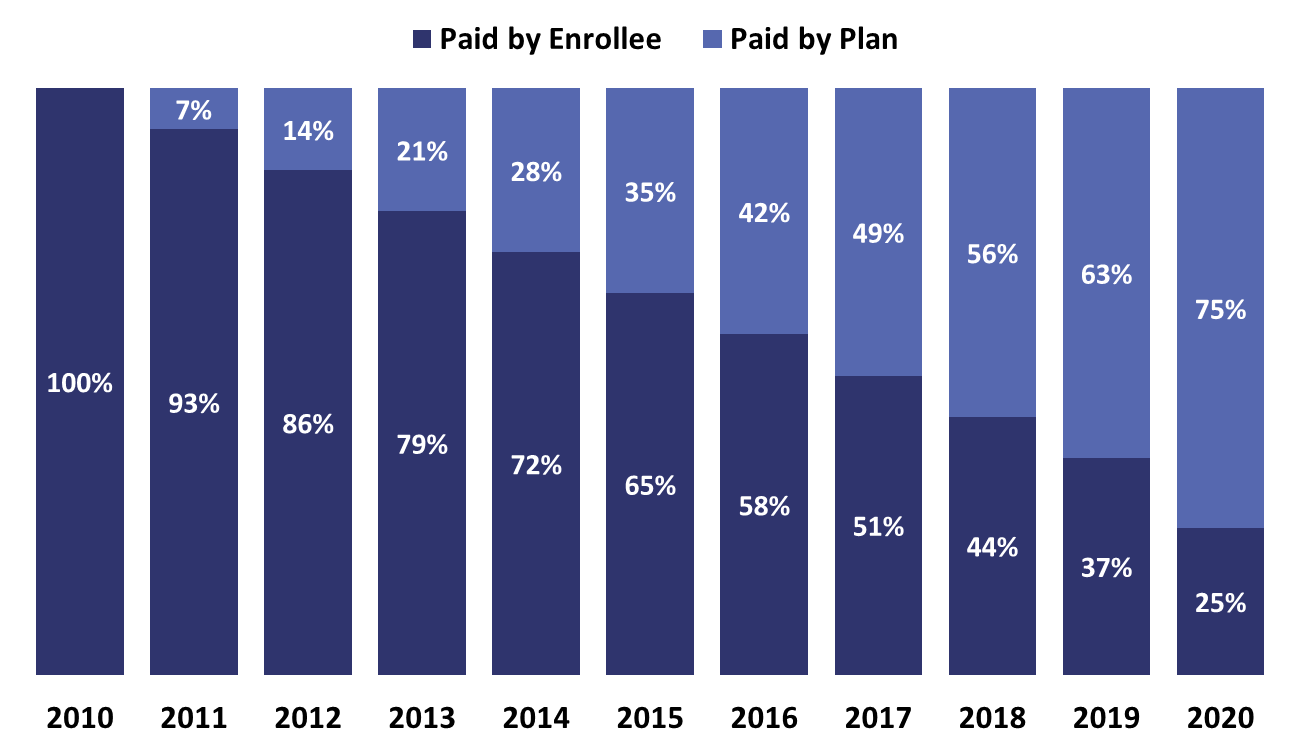

What is meant by the annual cost, annual spend, or estimated annual cost when we do a prescription drug plan (PDP) search on your behalf on Medicare.gov?

What is meant by the annual cost, annual spend, or estimated annual cost when we do a prescription drug plan (PDP) search on your behalf on Medicare.gov?